Inflation Doesn’t Have to Derail Your Retirement Strategy

Inflation is leading news headlines and it’s running at levels we haven’t seen in 40 years.1 In fact, the Consumer Price Index, which measures the rate of inflation, increased 7.9% in 12 months as of February 2022. Many Americans are worried about the impact inflation will have not only on their current spending but on their retirement strategy as well.

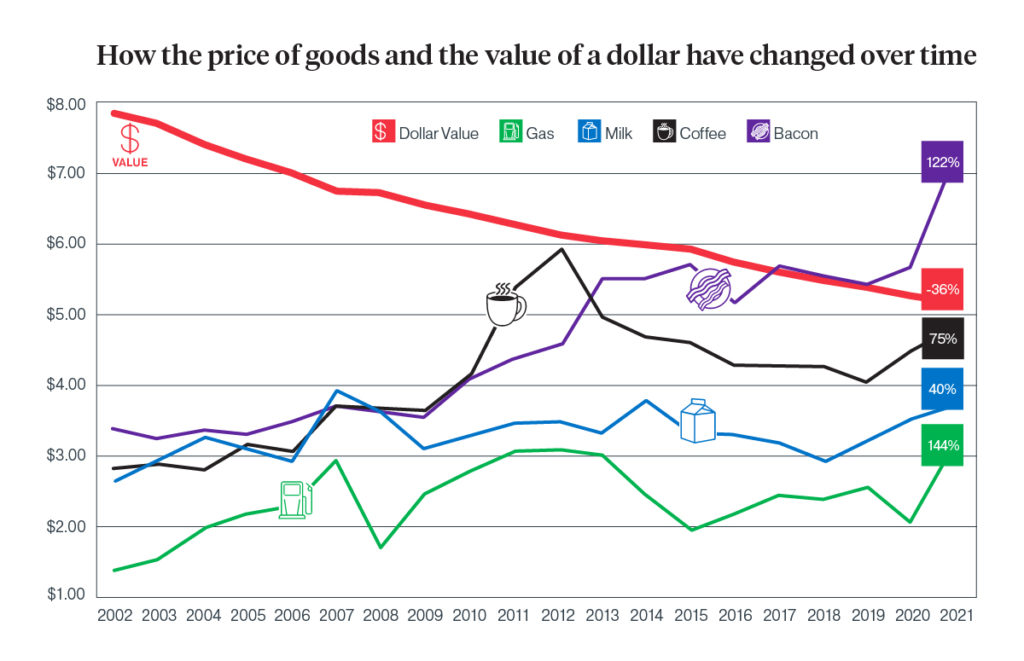

You’ve probably heard the saying “a dollar doesn’t go as far as it used to.” That’s because the cost of goods and services has consistently increased over time, leading to what we know as inflation. As you can see in the chart below, prices over the past 20 years have continued to increase — contributing to a decline in the purchasing power of a dollar.

The chart above is based on the Consumer Price Index for all Urban Consumers (CPI-U), which is widely used to measure the average prices of goods and services purchased by consumers.

So what does this mean for you and your retirement strategy? The higher the rate of inflation, the less your dollar will buy in the future. One risk is the potential to run out of money – a very real concern in light of the effect inflation can have on retirement income and the ability to cover essential living expenses. When inflation goes up, so does the need for more retirement income. When you’re working, wage increases can help you keep pace with inflation. When you’re in retirement, those increases stop but more income may still be needed to support your lifestyle.

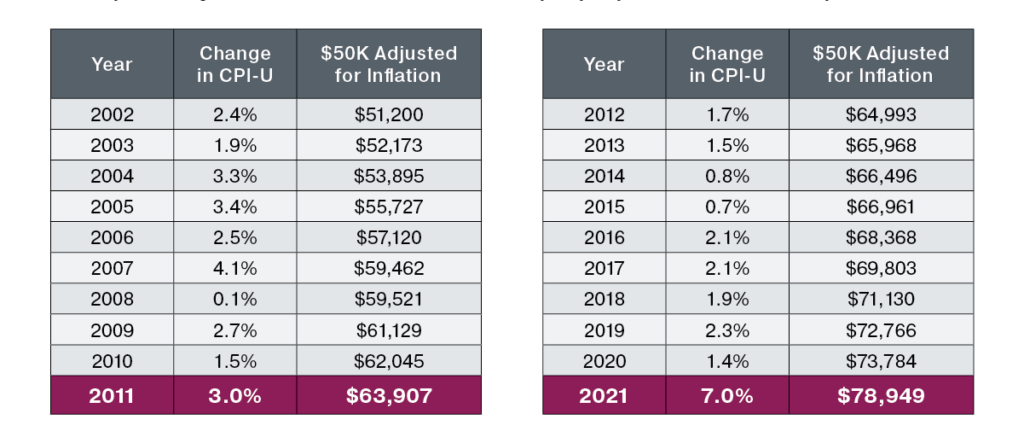

Take a close look at how your retirement income needs will change over the course of 20 years. Let’s say you need $50,000 a year at the beginning of retirement to meet your expenses 10 years later, you would need almost $64,000 to meet those same expenses. And after 20 years, you would need nearly $79,000. The 20-year average inflation rate is 2.32%. One dollar today may only be worth 64 cents in 20 years.

Annuities can be a key part of a well-designed retirement strategy and can help minimize the impact of inflation on retirement income, while providing a guaranteed stream of income.

Variable annuities are investment vehicles designed to help grow and manage retirement savings, so you can maintain your lifestyle throughout a long retirement. They can include features and optional riders like lifetime retirement income, flexibility and diversity through choice of investment opportunities for varying risk tolerances and asset categories and living benefit riders for growth, inflation and downside protection.

Indexed annuities are designed to help accumulate and protect retirement savings, allowing you to experience strong upside potential with downside protection. Some features of indexed annuities include retirement savings growth and protection and optional riders for guaranteed growth and protection.

You’ve worked hard for your money and there are steps you can take to help ensure inflation doesn’t derail your plans. Talk to your financial professional today to explore what inflation risk management options are right for you and your retirement strategy.

Source for all inflation-related data: The U.S. Bureau of Labor Statistics (www.bls.gov). Not seasonally adjusted.

1Historical Consumer Price Index for All Urban Consumers (CPI-U): U.S. city average, all items, index averages https://www.bls.gov/cpi/tables/supplemental-files/historical-cpi-u-202112.pdf

Optional riders carry an additional cost and some riders may not be purchased in combination.

An annuity is a long-term financial retirement vehicle, subject to market fluctuations. It may lose value, including the potential loss of principal, and is subject to certain fees and expenses not normally associated with other investment vehicles. Withdrawals are subject to contract provisions and will reduce the contract value, the amount used to calculate withdrawals or income payments and death benefit amounts. Withdrawals may be subject to income taxes and surrender charges and, when taken before age 59 1/2, may be subject to an additional 10 percent penalty tax.

Clients should consult their tax advisor before taking income or other withdrawals. If the annuity contract is held in a qualified account or plan, such as an IRA, the tax deferral feature provides no additional benefits beyond that provided by the qualified account or plan.

Any reference to the taxation of the products in this material is based on the issuing company’s understanding of current tax laws. Penn Mutual, its subsidiaries and its representatives do not provide tax or legal advice. Clients should consult their qualified tax advisor regarding their personal situation.

4288508CC_Feb24