How to Protect Your Retirement Income from Market Volatility Risks

You may already know how important it is to save for retirement and plan for your income to last as long as you need it to. But do you know that one of the keys to making that happen may be to diversify your sources of retirement income?

In retirement, you’ll experience the natural ups and downs in the market you may have experienced while you were saving for retirement. When the market is up, it’s a great time to take income from your investment accounts because they are commonly allocated to stocks, bonds and mutual funds—and tie directly to market performance.

What about when the market is down? When you take withdrawals from your investment accounts during a down market, your retirement funds will deplete more quickly and it will be harder for them to recover. This is why it’s important to consider having another source of income to rely on when the market is down.

This is where permanent life insurance comes in. In addition to death benefit protection, permanent life insurance can be a great source of tax-free income and serve as a safeguard against market volatility. Permanent life insurance can provide:

• Cash value that grows tax-deferred.2

• A source of income-tax-free retirement income.2

• Protection from market fluctuations.4

Taking income from your life insurance policy during a down market—instead of taking income from your investments—allows them to recover more quickly. It’s essentially like putting a bandage on your investments and giving them time to heal.

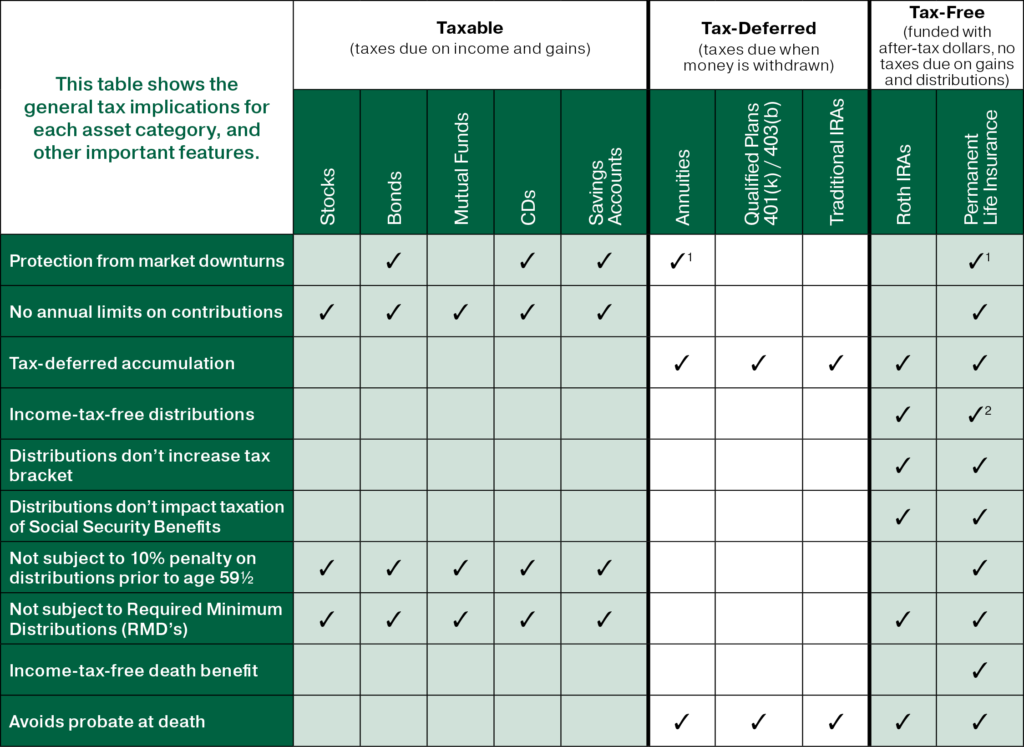

Having diversity in your sources of retirement income is one way to help meet your expenses and support your lifestyle. It’s just as important to diversify the taxation of your assets as it is to diversify the assets in your investment portfolio. From an income tax perspective, the assets in your portfolio can be categorized into three categories—taxable, tax-deferred and tax-free. Diversifying across these categories can help minimize the impact of taxes on your portfolio, helping to maximize your portfolio’s overall long-term growth.

Take a closer look at each asset category:

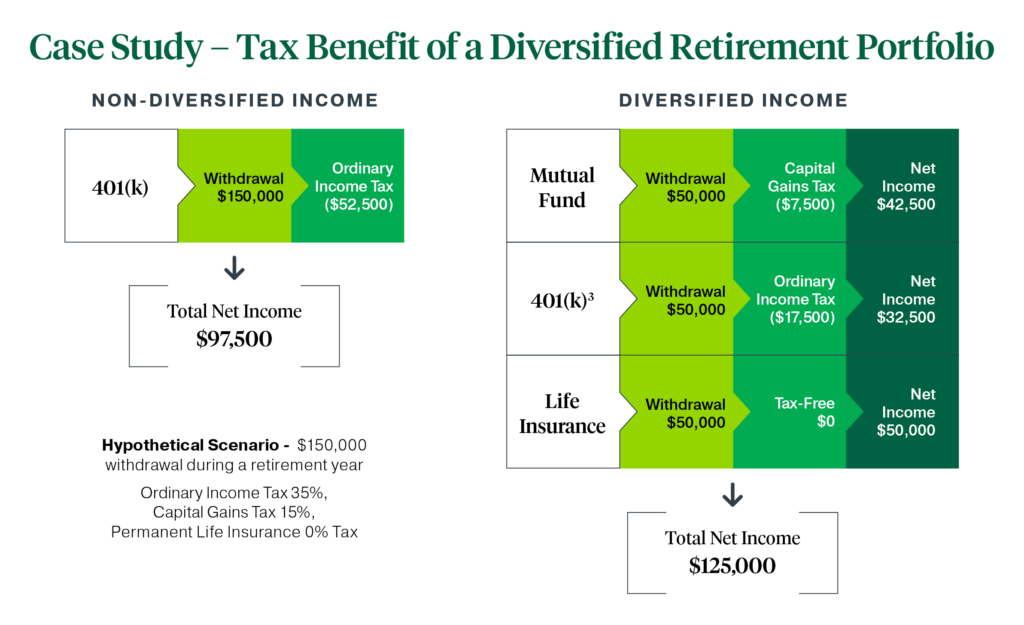

As you can see, life insurance can be a valuable addition to your portfolio, helping to minimize the impact of taxes and offering other advantages. Permanent life insurance is more than just death benefit protection. As a tax-efficient accumulation and protection vehicle that may help to safeguard against market volatility, permanent life insurance can be an important addition to any retirement portfolio as a diversified source of income. Let’s look closer at the tax benefits of a diversified retirement portfolio that includes permanent life insurance.

Life insurance can help minimize the impact of taxes in retirement and provide for your loved ones. Talk to your financial professional about how diversification strategies can work with your goals to maximize your income in retirement and help make sure your income lasts as long as you need it to.

1 With the exception of variable products, including variable annuities and variable universal life.

2 Accessing cash value will reduce your policy death benefit and values, may result in certain fees and charges and may require additional premium payments to maintain coverage. Ask your financial professional for details on accessing your cash value, including how it might impact the coverage guarantees and situations when the values you access could be taxable. Always consult your tax advisor before accessing a policy’s cash value.

3 The $50,000 withdrawal is post age 59 ½ and pre Required Minimum Distribution age.

4 Diversification does not ensure profit or protect against loss in a declining market.

The information in this material is for informational purposes only and is not intended as financial, tax or legal advice. Reference to the taxation of products in this material is based on Penn Mutual’s understanding of current tax laws. All guarantees are subject to the claims paying ability of the insurer. Depending on your individual circumstances, the strategies discussed in this presentation may not be appropriate for your personal situation. Always consult your financial, legal or tax professionals.

4969901CC_OCT24